- Stock Picker's Corner

- Posts

- Merck's "Six Pack" of Catalysts Have Moved it Toward the "Buy" Zone

Merck's "Six Pack" of Catalysts Have Moved it Toward the "Buy" Zone

Here's what coms next ...

Stock Picker's Corner (SPC)

March 11, 2026

In partnership with

When Big Pharma heavyweight Merck & Co. $MRK ( ▼ 2.37% ) unveiled a major reorganization late last month, I started a new “Wealth Builder Workup” on the once-great American drug company — for a six-pack of reasons:

No. 1: The stock was on my radar nearly two years ago as a “turnaround in progress” — a favorite “special-situation” play for Contrarian Wealth Builders like me.

No. 2: As part of our belief that “if you find the best storylines, you’ll find the best stocks,” Merck’s turnaround-in-the-making made it a possible beneficiary of our “Hunt for the Next Blockbuster” storyline.

No. 3: Merck is one of the “headliner” drugmakers careening toward the next big “Patent Cliff” – with more than $180 billion in drug sales now “at risk” by 2030 because of expiring patents.

No. 4: The readers of my old publication, Private Briefing, made big money on “Patent Cliff Plays” the last time around – including an 818% windfall from the takeover of blood-cancer innovator Pharmacyclics back in March 2015.

No. 5: I told you folks in late January that we’re jetting into a new “Patent Cliff Windfall Window” — with hefty windfalls from new rounds of buyouts and from the suitor companies who get those buyouts right — and that we’re hunting for Pharmacyclics-like opportunities for you.

No. 6: Spinoffs and other corporate breakups are among my favorite ways to profit. Merck’s restructuring is shaping up as a de facto breakup — albeit an internal spinoff as opposed to an external, public split-up. That could refocus the company — and perhaps lead to a “real” spinoff later on.

That “six pack” has moved Merck toward the “Buy” zone …

But is it an outright “Buy” yet?

Let’s take a look …

The Long Fall

When I took that look at Merck back in July 2024, I liked a lot of what I saw. It had a fairly new CEO — Rob Davis — and Davis was making progress. Merck was headed toward a “Patent Cliff” of its own — and was starting to make adjustments. And while it was losing one “Blockbuster” (a drug with annual sales of $1 billion or more), it had a new one that would replace at least some of the sales.

But I wasn’t ready to add Merck to our “Model Portfolio” — the list of our highest-conviction stocks.

It was the right call.

Merck closed at $128.66 that day. It’s at $117 right now. So Merck’s been “dead money” for two years.

Even then, I saw issues.

That “Next Blockbuster” — a pulmonary arterial hypertension (PAH) drug called Winrevair — generated sales of roughly $1.4 billion last year. But its peak sales are only forecast to hit $3 billion (Merck’s forecast) to $7 billion (other analysts) — and not until 2035.

But Winrevair won’t fully solve Merck’s No. 1 challenge: countering the 2028 patent cliff for its “Mega Blockbuster” cancer drug Keytruda, which topped $25 billion in revenue in 2023 — or about half of the company’s pharmaceutical sales. Sales of just that drug alone surged to $29.5 billion in 2024 and $31.7 billion last year. And industry analysts see Keytruda sales for this year hitting $33.6 billion.

Keytruda revenue will peak at a projected $35.42 billion in 2027 — and will contribute a still-hefty $33.7 billion in 2028, says FactSet Research.

But the loss of patent in early 2028 (as well as pressures from the Trump Administration’s Inflation Reduction Act) will hit drugs like Keytruda hard. Sales are projected to drop to $27.4 billion in 2029, a one-year decline of 19% — after which they’ll spin down enough to create a negative compound annual growth rate (CAGR) of 3.1% from 2025 to 2033.

As Merck’s leaders toiled to solve that “top line” issue, they decided to mitigate some of the bottom-line damage by cutting costs — chiefly through a workforce reduction that slashed 6,000 jobs, or about 6% of its employee ranks.

That move is projected to save the company about $1.7 billion from the cuts alone and an estimated $3 billion a year on an ongoing basis. But I’m skeptical. Remember, during my 20 years as a professional business reporter covering big public companies (and another 20 as an analyst, stock picker and financial columnist), I’ve covered the biotech “beat” several times. And many big restructuring initiatives with major companies in general.

Against that backdrop, I can say I’m unimpressed with how the Merck layoffs are being executed. We’ll watch to see if poor execution leads to operational slippage, manufacturing/supply-chain friction and internal (people and organizational) stressors — and if those execution issues show up as revenue misses, cost-savings walk-backs and (worst of all) profit shortfalls.

But some other moves — and this just announced corporate reorganization — have me intrigued.

Merck’s Wheeling and Dealing

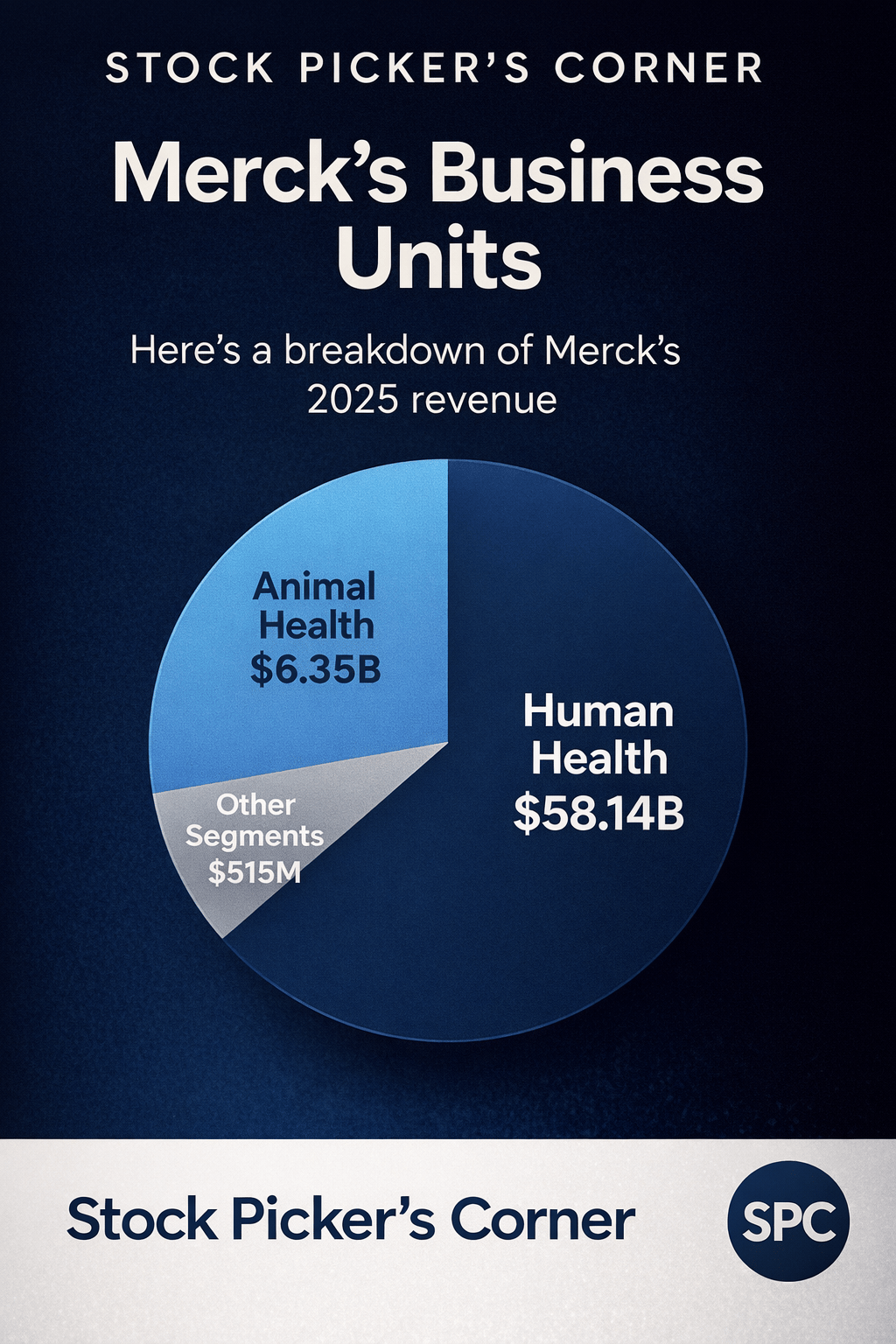

I’m super simplifying this, but Merck (2025 revenue: $65 billion) basically consists of two businesses:

Animal Health: About $6.35 billion in sales last year — or a bit more than 10% of total revenue.

And Human Health: This is Merck’s core pharmaceutical business and generated more than $58 billion in sales last year (or roughly 89.5% of total revenue).

And it’s the Human Health segment that Merck is reorganizing.

In its bid to steer clear of a total patent-cliff abyss — and to better focus on new drugs and those still in the pipeline — Merck is splitting that core pharma business in two: a focused oncology unit and then a separate one for other drugs, specialty therapies and infectious diseases.

The oncology unit will manage Merck’s inventory of current and experimental cancer meds, including Keytruda, which accounted for almost 49% of the company’s total revenue and nearly 55% of its drug sales last year. Despite that post-patent chasm, Merck execs have been combatively bullish about the post-Keytruda era, telling analysts they intend to “sustain [the company’s] long-term leadership in oncology.”

Vaccines and other non-cancer therapies — including Winrevair and the aging-but-dependable diabetes drug Januvia — will be housed in that second unit.

Over at least the last five years, Merck has been playing a Big Pharma version of the old Monty Hall game show “Let’s Make a Deal” to bolster its pipeline.

In addition to the deals outlined in the accompanying chart, Merck made such moves as:

1️⃣ The mid-2023 purchase of Prometheus Biosciences, a $10.8 billion deal that gives Merck a drug called MK-7240, which blocks an inflammatory protein called TL1A. The treatment is focused on ulcerative colitis and Crohn’s disease. And the technology also gives Merck immunology opportunities in other areas. It’s in late-stage testing but is still years from commercialization. Even so, the irritable-bowel-disease (IBD) market could be worth $50 billion by the end of the decade — presenting Merck with another growth pillar in its immunology business.

2️⃣ And the October 2023 Daiichi Sankyo ADC (antibody-drug conjugate) collaboration, worth as much as $22 billion, giving Merck worldwide co-development/co-commercialization rights for three DXd ADCs (HER3‑DXd, I‑DXd, R‑DXd). These are targeted chemo/antibody hybrids designed to treat breast, ovarian, lung and other cancers. ADCs are like “smart missiles” that can target specific tumors — without harming surrounding cells. The “DXds” are the smart warheads that can blast the tumor itself. These drugs are in different stages of testing. However, R‑DXd is a new first‑in‑class ADC aimed at certain ovarian cancers for which there’s no effective treatment. It’s actually earned the U.S. Food and Drug Administration’s special Breakthrough Therapy Designation after strong results Phase I, II and III trials. It’s not yet approved. But all these drugs could deliver on that Merck vow to stay out front with oncology therapies.

Which brings me to the “what comes next” for us …

Hunting for That Next Great Stock

Reports like this are part of our “process” here at Stock Picker’s Corner (SPC).

We find those great storylines.

We find the companies best-positioned to benefit.

We play the long game.

And we “Accumulate” along the way — turning pullbacks or regular cash investments to our advantage.

Our “Hunt for the Next Blockbuster” storyline will be supercharged by the looming Patent Cliff — which, as I said, I’ve seen before.

We’ll look for Big Pharma firms — like a Merck — that are buying smaller companies, unwanted units of like-sized rivals, focused product lines or new/in-development biotechnologies. Shopping sprees like that can jump-start the big player’s sales and profits — and we want to find the ones where that growth has multi-year “staying power.”

There’s another path, too: We’ll look for companies like Pharmacyclics that have terrific new technologies and that are innovative enough to break out on their own … or to make them buyout targets like the Mercks of the Big Pharma world.

The “end game” is simple: We aim to find “high-conviction” Wealth Builder stocks, or special-situation opportunities that can hand us shorter-term wins.

Merck is interesting as a possible turnaround — with a lot of the catalysts now lined up.

I’m also intrigued by the potential for this internal reorganization to end up being refocused externally. Could Merck look to spin off its animal health business or to break itself into separate oncology and immunotherapy companies?

We’re also hunting for those buyout targets.

I’ll keep you updated on Merck. Or you can use today’s report — and the first one referenced above — as a starting point for your own research.

If You Don’t Own These Stocks, You Should …

If we find some of those hotshot innovators, we’ll possibly add them first to our “Farm Team” — the roster of companies we’re reviewing for promotion to the “Big Leagues” … the Model Portfolio or the Special-Situation Portfolio.

One of our most promising breakup stocks is this one — which we just brought your way.

My top “Hunt for the Next Blockbuster” company is this one — which hit my first-year target-price forecast … right on the nose. And I see years of strong growth to come.

And let me mention one last stock that I’m super excited about. It’s a platinum-brand industrial company that’s planning a spinoff. And there are artificial-intelligence and quantum-computing “kickers.”

In fact, when I tell our readers about it I refer to it as “A Call Option on Quantum Computing.”

There’s still time to get some for yourself — before everyone else wises up to the massive potential. Here’s my latest update report — posted just last week.

We just celebrated our second anniversary here at SPC — which means we’re now in Year No. 3.

During that time, we’ve made some great calls — including a triple (plus some) on silver … a 393% gain (and counting) on this cutting-edge defense innovator … and this way-ahead-of-the-crowd forecast on AI power needs.

If “real income” suits you better, I just brought readers this stock with a 10.24% dividend. Better still: It’s like a “paycheck” stock — while most dividends are paid quarterly, this company pays monthly … so the payout comes 12 times a year.

I’m not boasting. I’m just proud of what we’ve done.

Because the work that we do … is done for you.

Join our community … subscribe below.

Folks who do … come to stay.

Explore More SPC Research | What SPC Premium Offers | SPC Premium Resources |

Privacy-first email. Built for real protection.

Proton Mail offers what others won’t:

End-to-end encryption by default

Zero access to your data

Open-source and independently audited

Based in Switzerland with strong privacy laws

Free to start, no ads

We don’t scan your emails. We don’t sell your data. And we don’t make you dig through settings to find basic security. Proton is built for people who want control, not compromise.

Simple, secure, and free.